By Mike Koetting May 26, 2026

This and my next post are on the American tax structure. The material draws heavily from The Second Estate, a superb book by Ray Madoff, a law professor at Boston College. I highly recommend it if the topic interests you. It is short and a surprisingly easy read. Her discussion covers much more than the items I am highlighting.

Payroll Taxes

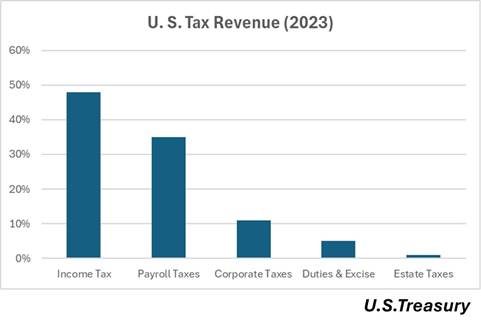

Today’s post focuses on payroll taxes, specifically Social Security and Medicare. I chose to start here because the problems of the income tax system often overshadow the issues around payroll taxes. To be honest, I had never given the matter more than a passing thought before reading her observations on the topic. I was surprised, for instance, that 67% of taxpayers pay more in payroll taxes than income taxes. All told, payroll taxes are the second largest source of federal revenue, comprising more than a third of federal revenue.

Still, people get confused as to whether payroll taxes are “real” taxes. In 2012, candidate Romney described the 47% of the population who pay no income taxes as freeloaders. But that isn’t the case. Most of these pay payroll taxes. When you include payroll taxes, the number of people not paying some federal tax drops to 16%–and most of those are still paying state and local taxes of one sort or another. (Since 2012, the percentage of people not paying any income tax has dropped from 47% to 40%.)

Payroll tax is 15.3% of the wages or payment in lieu of wages. This amount is subdivided between support for Social Security (12.4%) and parts of Medicare (2.9%). The amount of payroll taxes rises directly with wages, sort of. Employed individuals pay only half this amount (7.65%) in the form of a deduction from their salary; the other half is paid by the employer. However, economists broadly agree that employer payment of these taxes holds wages down, so it’s not exactly “free”.

Self-employed people pay all 15.3% themselves. For gig workers and independent contractors, this means that, for example, of the first $60,000 they earn, more than $9000 will go for payroll taxes. Additionally, payroll taxes are calculated on the full amount of the earnings, even though some of those earnings will most likely be paid to the Federal government in the form of income tax.

Social Security taxes only apply to the first $168,600 of earnings. While $168,600 is a healthy income, about 6% of the population earn more and, since, by definition, those are high earners, about 17% of the nation’s wage earnings fall outside this limit and are, therefore, not subject to Social Security taxes. It is also the case that some types of income fall outside payroll taxes. For instance, limited partners and owners of S-corporations largely avoid payroll taxes on a significant share of their income. These exclusions are in addition to the 17% of wages that are not subject to Social Security taxes. To add insult to injury, many of the nation’s richest people do not get compensated by wages and do not even hit the $168,600 cap. Elon Musk and Bill Gates, for example, do not receive compensation through wages and pay nothing toward Social Security or Medicare, two of the nation’s top three expenditures. I doubt they are worried they will not be eligible for those benefits.

Moreover, because payroll taxes are less obvious to the public, Congress has been able to raise them with less outcry. Since 1970, payroll taxes have more than doubled while the top income tax rate has fallen from 70% to 40% and estate taxes, once 77%, have become immaterial in many cases because of lower rates and various loopholes that exempt funds from taxation. (More on that in the next post.)

Problems Ahead

On the other side of the equation, at any given time, about one in five Americans receive some form of Social Security benefits. These benefits help stabilize the economy by providing support for the retired and for people not capable of working. Without these benefits, not only would the recipients be hurt, but the decrease in expenditures made by or on behalf of recipients would adversely impact various sectors of the economy.

Unfortunately, the Social Security Trust Fund is steaming towards insolvency. This is currently projected to happen in the early 2030’s, just six or seven years from now. Under current law, this will require a material reduction of benefit levels for everyone. Although people are often confused on the point, there is no accounting link between money an individual puts into the fund and the benefits paid out. Social Security is a “pay-as-you-go” bucket. Each year taxes are paid in and benefits are paid out. Historically, this has worked well because increasing wages and population growth, the latter partially fueled by immigration, meant the fund has always been able to cover benefits and, typically, leave a surplus for future years.

But the world is changing. Older people are living longer and population has stopped growing—fewer children and kicking out immigrants. In 1960, there were 5.1 workers for every beneficiary. Today, it is 2.7 and that ratio will continue to decline. Without other changes, the surplus that has sustained the fund will be exhausted. The total pay-in is estimated to be about 83% of current benefit levels. Existing law mandates that if the pay-in sum falls short of the pay-out rate, all benefits should be reduced on a pro-rata basis to equal the pay-in sum. Reductions could, therefore, be larger if revenues decline faster than anticipated or additional benefits are paid out. (Trump’s Budget Bill, for instance, reduced revenues for the Trust Fund because in giving a tax break to some seniors, it curtailed revenue to the Trust Fund. This is not the biggest issue but is estimated to accelerate the insolvency of the Trust Fund by six or so months.)

One would think Congress would be all over this issue. More than 80 percent of Americans oppose any benefit cuts. Even among high income groups, those most likely to believe benefits should be cut, 73 percent oppose cuts. The current lack of serious Congressional discussion is huge cause for concern. This issue needs to be addressed much sooner than later. Any fix will require some time to negotiate and implement. As the American Academy of Actuaries points out, if reforms are left until the last moment, they might well require more drastic actions.

The lack of action is not from lack of alternatives. The problem is a lack of will in our constipated Congress. It is highly likely that whatever happens will cause someone to be unhappy. Generally, Democrats want more revenue and Republicans want to cut benefits. For better and worse, neither side has enough votes to impose its vision on the other side. The overall toxicity of the environment makes the kind of compromises necessary hard to the point of impossible. The problem is further acerbated by the fact there is a material group of Republicans who keep trying to find ways to privatize Social Security, despite an amazingly broad opposition to the idea.

Most likely solutions—if any can be reached– will impose some mix of greater revenue and changes in benefits. The Brookings Institution has circulated a thoughtful proposal that in normal times could be the basis of a bipartisan appeal. As would be expected on issues this major, the proposal is complicated and resists easy summary. It includes about 15 separate elements and has proposals that raise revenue, including raising both the tax rate and the taxable ceiling, and working to increase legal immigration, but also increasing some benefits and shaving others. The specifics of this proposal aren’t necessary for this essay—not only are they very wonky, but there are surely other proposals with equally plausible specifics. The important point is that there are solutions that could avoid a catastrophe, should Congress choose to accept its role.

The situation with Medicare is similar to the problems in Social Security. Medicare’s financing structure is actually more varied than Social Security. Medicare has several different sources and funds. But the Medicare portion of the payroll taxes that supports Medicare inpatient care is heading for the same rocky shore as Social Security. It will also be broke in the early 2030’s for the same reasons, fewer people paying in and people living longer. It is further fighting a headwind of healthcare costs rising faster than overall wages, thereby making it harder for payroll taxes to keep up. A similar set of solutions is required on roughly the same timetable.

Inevitable Conclusion

There is little market in today’s American political scene for proposals with complicated moving parts. But any proposal that isn’t multifaceted is going to increase material problems elsewhere in society. Time is running out. Without Congressional leadership and a Chief Executive willing to support the kind of negotiation necessary, this problem will not be solved. In other words, we’re stuck till at least 2029. Those who depend on Social Security should be worried, very worried.