By Mike Koetting June 9,2026

This post is the second of two on the American tax structure. The previous one focused on payroll taxes; today’s post addresses other taxes. Again, the material draws heavily from The Second Estate, a superb book by Ray Madoff, a law professor at Boston College. I highly recommend it if the topic interests you. It is short and a surprisingly easy read. An even shorter version of her thinking is available in an interview with Erza Klein. Today’s post is not trying to summarize what she said but to focus on the macro implications.

****

The title of Ray Madoff’s book, The Second Estate, refers to the official distinctions in prerevolutionary France between the three strata of society—clergy, nobles and commoners. Members of the Second Estate, the nobility, enjoyed special privileges, which included freedom from taxes. She suggests that the wealthiest people in America have created a new form of the Second Estate.

It is common knowledge that today’s economy features an economic distribution as extreme, probably more extreme, than the Gilded Age at the end of the 19th Century. However, the difference between the top and the bottom is so large and the labels thrown around so much that it is easy to lose track of how great those differences are.

Madoff places it in perspective by using a time metaphor to help understand how wealthy today’s wealthy are. One million seems like a big number. One million seconds takes about 12 days. One billion seconds, however, takes 31 years and one trillion seconds requires 31,688 years. Today there are about 900 billionaires in the United States and their wealth grew by about 18% in 2025. There is currently one trillionaire and about half a dozen who could achieve that status in the near future. The difference between even the millionaires and the billionaires is almost unfathomable.

Like most people, I believe we are not taxing the richest sufficiently. Embodied in that statement are two suppositions. First, the current level of governmental deficits does not generally result from profligate spending but from insufficient taxes to meet the full range of the country’s needs. (Of course there is some inefficient spending and it should be addressed; but contrary to the palaver generated by the likes of Musk and Heritage Foundation, those issues are not at the root of the problem.)

Second, this shortfall in revenue should primarily be made up by those with the most resources. In part because their resources are so astounding as to cease making human sense and in part because doing so improves social cohesion. None of this suggests a complete flattening of the income distribution—which attempt would be deeply counterproductive. As is shown in an instructive infographic, the American people have a widespread sense that there should be demonstrable differences in the distribution of wealth. They recognize both that it creates incentives that can benefit all and that there is an underlying fairness in greater rewards for great contributions. However, there is wide and deep opposition to the extremes of the current distribution. Too much of a useful difference is too much.

We All Know How We Got Here

During the middle of the 20th Century, America had a social ethic that promoted sharing the benefits of productivity growth with the entire population. This included a broadly redistributive tax structure. But the titans of capital wanted more. (One should never forget John D. Rockefeller who, when asked “How much is enough?” said “Just a little more.”) From Ronald Reagan on, there has been a persistent, and largely successful, effort to reduce the relative burdens of taxation on the richest. At the same time, shifts in production functions have resulted in ever greater shares of the nation’s economic growth winding up in the hands of the owner of capital.

Madoff’s book outlines how the American tax system—despite its generally progressive structure–has pockets of inequity so great as to change the nature of the country. To oversimplify her story, what has happened is that Congress lost its nerve and allowed, in the fog of the tax code, the nature of income to be redefined in so many ways that if you have enough money, your income for tax purposes shrinks.

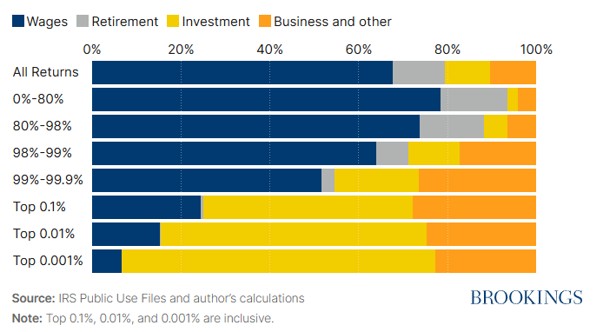

The below chart from the Brookings Institution on sources of income across the total distribution gives a flavor of the issue. As is readily apparent, for the bottom 98% of the income distribution, about 90% of income is from wages or retirement income and is subject to regular income taxes, which are progressive. But at the very top of the income distribution, wage income is a relatively negligible portion of income. To be clear: income not in the form of wages is not necessarily tax free. But it is subject to a variety of different taxes, almost all of them with lower impact than if the tax had been calculated at the nominal income tax rate.

And if a graph doesn’t make the point, how about a lurid ad hominem anecdote. Since the 1990’s, Jeff Bezos salary has been capped at $82,000. This salary is low enough to make him eligible to claim the child tax credit, which in fact he has. But from 2014 to 2018 his net worth climbed by $99 billion. (Remember, in time terms this is equivalent to about 3000 years when one million is only 12 days.) However, he paid less than one billion in taxes, or about 1%. Now a billion dollars is undoubtably a lot of money. But this percent is considerably lower than most middle-class families pay. Moreover, it is inconceivable that two, five, or even twenty times that amount would make any difference in his lifestyle. Nor would taxes at higher rates have any appreciable impact on the incentive to make lots of money…err…I meant, grow the economy.

Corporate Taxes

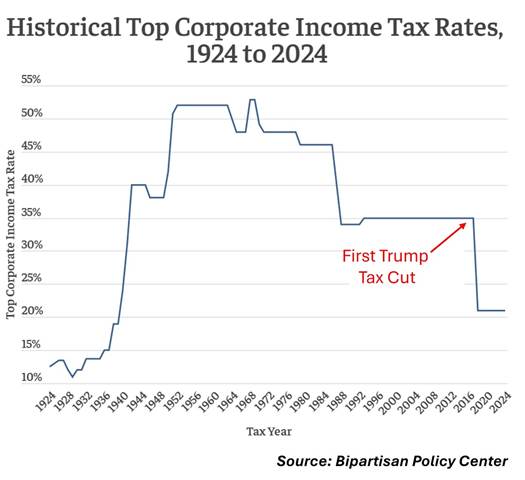

The literature on corporate taxes is particularly contentious. Many respectable economists are willing to consider the possibility that raising corporate taxes is a drag on business, particularly those that compete in global markets where other countries have lower corporate taxes.

Indisputable, however, is that American corporate tax rates have declined materially, most recently as a result of the reduction in the 2017 Trump tax cuts. From a mathematical perspective, that appears to have had a large adverse impact on the deficit. The question is whether giving corporations more money improves employment by greater than offsetting amounts, as apologists for the cuts contend.

Recent research suggests this did not happen for the 2017 cuts. While there was some positive business growth, it was not nearly enough to offset the increase in the deficit. Note, part of the issue is there were also a number of detailed changes in the tax code that, on balance, also gave more money to corporations. Nor did it stop in 2017. By executive order, Trump made it easier to attribute earnings to low tax countries, resulting in at least a $40 billion windfall for American multi-nationals.

Inheritance Taxes

Madoff has special scorn for the spinelessness Congress has shown in allowing the inheritance tax to be whittled down to the point that for many of the richest families, it is negligible. For years rich people sought loopholes to the inheritance tax. And, of course, loopholes were found. But Congress would periodically review the taxes and close loopholes. Now Congress has not only stopped closing loopholes, it has systematically lowered thresholds and created new loopholes.

I can’t imagine a policy rationale for this course of action. Some degree of leaving resources for your family is something a society should protect. But how much? In the 2023 Forbes list of the 400 richest people in America, more than 30% were on that list not because they started a business that benefited society, but because they had the good fortune to be born extremely rich. And, while surely many of these are using their wealth in beneficial ways, given the competing needs of society, how much headstart do we want to give to the offspring of the wealthiest? What evidence is there American society thinks creation of a class of virtual nobility is a good idea?

Where From Here

It is unlikely there is a bumper-sticker solution. The simplest ideas often have the greatest number of hidden effects. Madoff, for instance, is not a fan of wealth taxes—difficult to administer and potentially unfair because of fluctuating value of investments. But she is fully in favor of some mix of provisions that put investment income on a more equitable footing with other income and, particularly, that removes many of the tax benefits of inheritance. (One high priority for her would be removing the “step-up“ provision, which she calls the “Angel of Death Loophole.” This currently allows accumulated holdings to be transferred to heirs tax free. She argues that, as Canada does, wealth at a person’s death should be treated as realized gains and taxed accordingly before being passed on. According to the Congressional Budget Office, adopting something like the Canadian approach would generate about $200 billion over the next decade.)

Whether or not it gets adopted, the discussion of a “wealth tax’’ has put the issue squarely on the table. From my perspective, the issue now is to get beyond this as a slogan and have an honest discussion as a country as to what we want from our tax system and then how best to get there. There are plenty of specific provisions that would get us closer to where the vast majority of Americans think we should be—and which, cries and hysterics not withstanding, will not cripple the economy. It is certain that any specifics will have some drawbacks, but perfection is not necessary. What is necessary is a tax system that the bulk of Americans think is fair and that produces enough revenue for the things those same citizens want the government to provide.

Historically, we approximated that because the adult members of Congress would periodically dampen their partisan differences and hash out something that would work. At least for a while. Rinse and repeat. But for a variety of well-known reasons, that’s stopped working. The result has been general capitulation to the rich.

It has always been the case that the richest have the loudest voice. Surveying the damage of the Wall Street crash of 1929, 95 years ago, Drew Pearson, describing the leaders of Wall Street, said: “For them, the door of the White House, of every Cabinet member, is always open. But it is exactly this that makes their influence so powerful, their position so dangerous.” Citizens United has solidified the sway of the richest in a way that no historical precedent could have predicted. In the 2024 presidential election, 44% of the donations to Trump came from 10 people. Democrats also benefited from megadonors, just not as much. As Brooke Harrington, a Dartmouth professor has said, today’s billionaires have become noblesse without the oblige.

The results, however, are unstainable. If Congress does not find its missing backbone, either the rising deficit strangles the economy or we wind up, one way or the other, where the French Second Estate eventually ended.