By Mike Koetting February 14, 2023

In my last post, I suggested that a substantial revision of America’s tax code might be a meaningful step towards bridging our national divides. Today’s post proposes one specific change in the federal income tax. There are several other critical tax issues that need to be considered, but those are for another day.

The essence of today’s proposal is to materially expand the use of the Alternative Minimum Tax against a different definition of income than is currently the case. The resulting tax laws should be able to be clearly explained and understood by most people as actually collecting higher taxes from those who are better off. More concretely, the goal is to increase the total income tax collections, with all of the additional revenue coming from people who earn more than 250% of the median income and use all the proceeds to reduce the deficit. (In 2022 a family income of $200,000 or above is roughly 250% of the median income, approximately the top 10% of incomes.)

A reminder. This proposal is about increasing social solidarity through modest fiscal sobriety. At bottom, I believe the lack of social solidarity may be the country’s biggest problem. This distrust is brought on by a large number of social changes that are not likely to be reversed. So we must find a way to rebuild trust in the collective using a different model than we find in our history.

This is not meant to address all the serous issues the country faces. In particular, my proposal is not specifically aimed at addressing income inequities–although it would have a favorable impact in that direction. The degree of inequality is a very serious problem and certainly contributes to our national malaise. But its causes are multiple and complex. Even a more radical overhaul to our tax structure cannot by itself solve that. I would like to see those changes, but while I am waiting, I am proposing a change in our income tax that is within the current framework.

Background

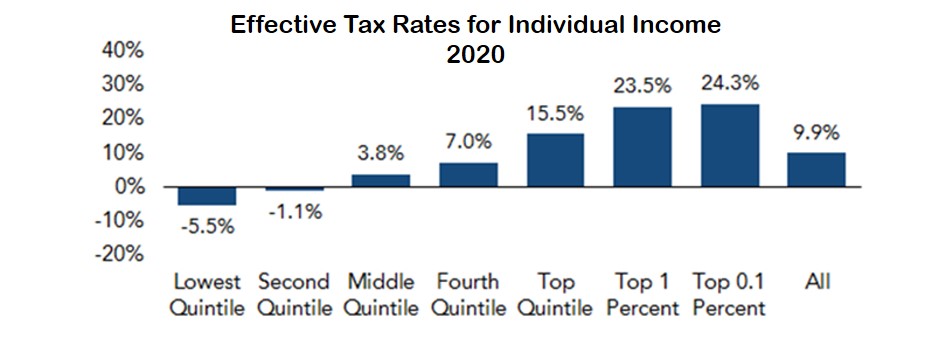

While the total tax structure encountered by citizens is very barely progressive, the Federal income tax is relatively progressive. It is not as progressive as one might expect from the nominal tax rates by bracket. But even when looking at the effective rate, it is clear that on average the more income you have, the higher your taxes. The tax rate for the highest 1% is six times the rate for the middle quintile of taxpayers and 3.5 times more than the next quintile. (The effective tax rate for the bottom two quintiles is negative—that is, they receive more credits than any taxes they might owe.)

Source: Tax Policy Center (Urban Institute -Brookings Institution)

On the other hand, the actual income taxes paid can vary quite bit from individual to individual, even if they have the same basic income. This is because, for reasons good and bad, some kinds of income have received special treatment in the tax code. These provisions are why some individuals with high incomes have low taxes.

The Alternative Minimum Tax (AMT) is found in the complicated thicket sprouting in these provisions. It was created in 1969 as a Congressional reaction to evidence that some wealthy people were able to string together various deductions and pay no taxes. The AMT works by requiring tax payers with income over a certain threshold to make a second calculation. The second calculation is made by adding back some of the otherwise allowable deductions and then multiplying by the AMT rate. The tax liability is the higher of the two. The AMT rate has only two brackets–one at 26% and the other at 28%.

How much difference this makes to tax receipts depends on what deductions are returned to the base before calculating the AMT. After the Trump tax cuts of 2017, the AMT applies to only 0.1 percent of taxpayers, and is particularly weak against the highest incomes. Under current law, those changes will expire in 2025 but even so, the Tax Policy Centers projects that fewer than 4% of taxpayers will have their liability calculated in this manner.

Proposal

My proposal has three parts.

- Returning more possible liabilities to the base for calculating the AMT. All things being equal, that would lead to higher tax liability because the base against which the AMT was calculated would be higher.

- Setting a rate for the AMT which would result in aggregate tax revenues from those with incomes over $200,000 to be roughly 50% more than they are now. Getting to a specific aggregate amount is a key part of the proposal.

- Using all additional proceeds to reduce the deficit. (Using them for other things would inevitably pit various groups against each other.)

Explication and Complications

The most obvious is that a 50% tax increase for the richest 10% of Americans would most likely create a truly spectacular political firestorm. I am not sure how much of a disadvantage this is if one of the goals is to further the cause of increasing social solidarity. Support for this proposal would not be simply along party lines. People are uncomfortable with the size of the national debt. Despite their ongoing saber rattling about the size of the deficit, Republicans are proposing a range of income tax changes that will be make the deficit even larger. Similarly, as was starkly clear at the State of the Union address, proposals to reduce the deficit by cutting Medicare and other social programs have no political traction. Viewed in contrast, an explicit proposal to attack the deficit by taxing the rich makes it crystal clear what are the actual motivations.

Moreover, it is equally clear that in the years since the Bush tax cuts of 2001 and 2003, income inequality has spiraled. Since 2000, median income (adjusted for inflation) has risen by 6.7%. But the income of the top 10% has risen by more than 20% and the top 5% by more than 25%. Income for the top one percent, which has a huge share of potential tax liability, has grown still more.

My back-of-the-envelope calculations suggest a 50% increase in tax liability would increase the effective tax rate for the top 10% of incomes to somewhere just below 40%. This is very similar to the current nominal tax rate. There will still be enough difference between the after-tax income of people in these brackets and the rest of the population that it will be hard to stomach the inevitable argument that it will stifle ingenuity. (The difference between the top and middle in the American income distribution is colossal; anything short of outright confiscatory taxes can’t erase that canyon.) To be sure, if enacted, there will be some people with high tax liability leaving the country. But it will raise the question of just what do individuals who succeed fabulously in the United States owe to the country.

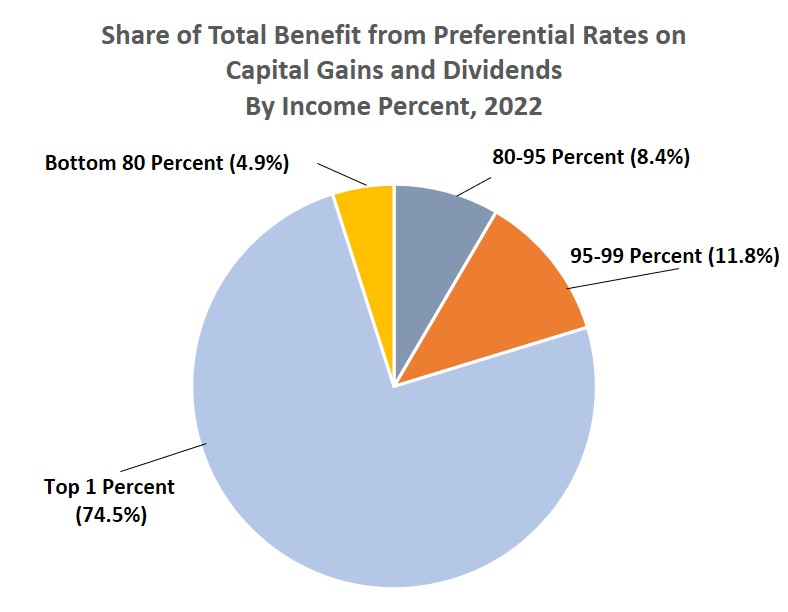

Another whole line of consideration is the question of which existing deductions to use in the calculation of the AMT. It is possible to achieve a particular aggregate amount in a multitude of ways. But each of those routes will create different winners and losers. Some of the changes could be dramatic. Accordingly, it is fair to assume, in addition to a general opposition to this proposal, there would be bloody internecine war among the rich to keep their favorite deductions outside the AMT calculation. I don’t see any reason to pick favorites in that contest. Although advocates for one or the other will surely find a disabled veteran farmer in Nebraska who would be adversely impacted by some provision, it is clear that most of these special deductions are for the better off. By making the target an aggregate amount, these arguments make a difference only to high tax payers

Source: Tax Policy Center (Urban Institute-Brookings)

My proposal would not “solve” the deficit. By another of my rough calculations, this will raise about a trillion dollars annually (based on the 2021 tax revenue). Over 10 years this will make a meaningful dent. While it will still be necessary to police the size and direction of the deficit, we could be less hysterical about it.

More important, in my view, is that it will send two useful messages:

- Government can work to make changes that advance the whole society, not just special interests.

- There is a commitment to fiscal sobriety. This should provide some modest comfort to people approaching retirement age and to young people, who are concerned about the fiscal mess we are leaving them.

Perhaps I am overly optimistic, but I think these two messages would be a meaningful start in improving trust in government. They certainly wouldn’t solve many of the problems facing America. With no other changes, the impact on economic inequality would be modest. And many of the other divisive issues facing the country are cultural and will require changes much broader than can readily be achieved through policy tinkering.

Even if this proposal is just a spit in the bucket of our national problems, it is a bold step in the right direction. And it just might be possible.