By Mike Koetting January 17, 2023

Having neither a degree in economics nor a crystal ball, I lack the proper credentials to post a blog on inflation and the Federal Reserve Board. But the issue is very important to the well-being of the society—probably more than most of us acknowledge–so I will take my chances.

The Issue

The Federal Reserve Board has evolved the responsibility of steering the national economy between two potential disasters, runaway inflation and recession, another hell or high water situation.

Runaway inflation is deeply corrosive of society. If your income—be it paycheck or pension—suddenly stops supporting the life you expect, you get grouchy. Majorly. It seems like the fundamental contract between you and society has broken down. Chaos often ensures.

But cracking down too hard on inflation can create a recession. Unemployment grows, workers no longer feel empowered to ask for raises and sellers are wary of raising prices. Less chaos, unless the recession becomes too steep. But as much—maybe more—human suffering.

As a practical matter the Fed has only one tool for steering, tightening or loosening credit. There are multiple factors that determine inflation in the economy so ratcheting credit up or down is kind of a blunt instrument. As a consequence, it has to be used very judiciously if it is to reduce inflation without creating a recession.

Regarding the country today, it seems that the Fed has been threading this needle pretty well. Inflation is moderating and the labor markets are still strong, as evidenced by the unemployment rate edging down last month to its lowest post- pandemic level. Central to this navigation has been a series of interest rate increases, seven raises since March, 2022 from 0.25% to 4.5%. The question now confronting the Fed is how to extend their success thus far in reining in inflation without inducing a recession– and what course of interest rate adjustments can achieve this end.

I will not be so foolish as to pretend to know what the Fed should do. This is their day job. But there are a number of considerations that might be of interest.

How High Is Inflation?

The measure of inflation that gets the most press is year-over-year inflation. That is, how much higher are prices today than they were a year ago. As useful as this is, like most statistical measures, it has limitations.

In particular, if there is a singular price spike in a short period and the prices established that month stay at the higher level, the annual measure of inflation will be influenced for the entire year. The economy may be stuck with that inflation, but there is no ongoing problem that needs to be blunted.

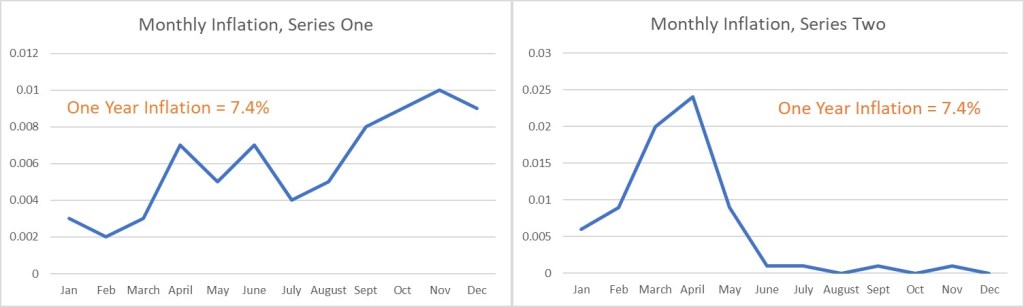

The below graphs show two hypothetical courses of inflation on a month-by-month basis for a year. Both these imaginary economies reflect a one-year inflation rate of 7.4%. But the patterns are very different. One shows a generally consistent upward inflation rate. The other shows a strong inflationary shock at the beginning of the year, with very little inflation the second half of the year. The more consistent pattern suggests a generalized “overheating” of the economy (disposable income driving up demand beyond the economy’s ability to keep pace). The second suggests a more discrete event or set of events that created price spikes that may well be resolving themselves.

Needless to say, reality may not sort itself into such obvious buckets. Reality is further complicated as various sectors of the economy can be inflating (or deflating) at different rates. But these illustrate the issue in choosing what inflation to consider.

Again, I am not licensed to offer an assessment that you could take to the bank of what the current situation more closely resembles. Indeed, there is a fair amount of debate among those people who are appropriately licensed. But after reading a bunch of these arguments, it sure looks to me more like our inflation spiked last winter/spring. From June, 2022 to December 2022, the month-over-month inflation rate was at the low end of the range of pre-pandemic normal. So when the New York Times reports the annual inflation in December at 6.5%, it is not wrong. But it is also not necessarily complete.

The Fed needs to be very careful if it is to avoid nudging the economy into an unnecessary recession.

Implicit Biases

Federal Reserve Board Chairman Powell is very fond of saying that the Fed is above politics. In the narrower sense of the term, that is absolutely the case. Even with a slightly broader definition, he has been willing to take positions without regard to partisan considerations. But politics doesn’t stop at the border of partisan differences. Making decisions about which risks to prioritize over other risks inherently reflects politics in the broadest sense of the term—how as a society we make contested decisions that impact the entire society.

Neither excessive inflation nor a recession is in anyone’s interest. But slowing down the economy by making credit more expensive will inevitably “soften the labor market,” as Chairman Powell concedes.

We should ask who takes the brunt of the hit when the labor market cools off? Every one suffers but those who lose their jobs or forego increases in income suffer the most. For the last couple months, I have been fascinated that the stock market retreats when continued job growth is reported. The standard line is that is a consequence of Wall Street fearing another rate hike by the Fed. But it occurred to me, there may be a more parsimonious explanation: a tight labor market means workers have more bargaining power, which will put pressure on company profits.

For the last 40 years, wages for most workers have grown more slowly than the overall economy. Right before Covid and as we have been coming out of the Covid period, worker salaries have made some real gains. To be sure, some of those have been undermined by inflation. But given that the bargaining power of unions has been so badly undermined during those 40 years, the vision of collective bargaining inflaming inflation by holding out for anticipatory price increases—a real problem in the 80’s—may be largely outdated.

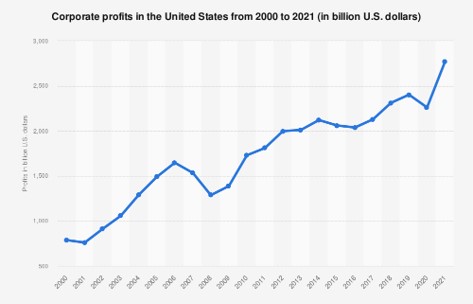

We may be facing a very different problem. Sources as divergent as the Economic Policy Institute and Bloomberg have pointed a finger at the role of corporate profits as a major factor in contributing to inflation. Oil companies, for instance have posted record profits while Republicans made blaming Biden for high gas prices the centerpiece of their midterm campaign.

U.S. Bureau of Economic Analysis, Statista 2023

To the extent cranking up profits is a culprit in inflation, increasing interest rates will have less effect on the rate of inflation. But a softer labor market will certainly reduce worker leverage.

How Much Inflation Is Too Much

For the last several decades, the Fed has had a target inflation rate of 2%. Economists Robert Pollin and Hanae Bouazza have suggested that this target may be overly aggressive and we may be paying a considerable cost in terms of lost economic activity to bring inflation down that low. Their chart, shown below, suggests that real GDP growth has been highest in years with an inflation more in the 2.5 – 5% range. This is consistent with the same analysis for 37 high income countries.

I am relatively sure there is other economic literature that takes issue with these numbers. Although virtually all economists recognize that there are real trade-offs between growth and controlling inflation, a target rate this high is certainly not in the mainstream of economic thinking. Still, it is worth considering on what basis the 2% target is determined.

What to Do

I can’t think of much that the average person can do. While I am currently worried that the Fed may be too focused on controlling inflation, I am also aware that once inflation really takes hold, it can be hard to stamp out. Stopping an antibiotic prematurely leads to more potent infections. I just don’t know enough to have a strong opinion.

I certainly don’t think the situation would be improved by making interest rate decisions overtly political. Although it is without question that the decisions are profoundly political in their impacts, I would still rather have the relatively impartial Federal Reserve Board—implicit biases and all—making the decisions. So far, at least, they seem to be doing a reasonable job.

I think the best we can hope for is that academics keep debating the issues. They need to make sure that they listen to arguments outside whatever orthodoxy is reigning at the time. Thoughtful and lucid journalistic coverage helps, but am not sure that the mainstream media has done as good a job as possible making these issues clear. Robust and open debate will improve the odds of avoiding a huge mistake.

*******

NOTE: Thanks to Ira Kawaller for reviewing an earlier draft of this blog. His advice was very useful, but he can’t be blamed for my opinions or errors. If you are interested in a blog that offers political economic analysis in a short, lucid and intelligible format, I highly recommend his work. Read him at igkawaller.medium.com.